Table of Contents

Filed Pursuant to Rule 424(b)(4)

Registration Statement No. 333-233198

Registration

Statement No. 333-233963

PROSPECTUS

6,620,686 Class A Common Shares

Global Ship Lease, Inc.

Class A Common Shares

We are offering 6,620,686 Class A common shares in this offering.

Our Class A common shares are listed on the New York Stock Exchange, or the NYSE, under the symbol “GSL.” On September 26, 2019, the last recorded sale price of our common shares on the NYSE was $7.76.

Investing in our Class A common shares involves a high degree of risk. See “Risk Factors” beginning on page 23 of this prospectus for a discussion of information that should be considered in connection with an investment in our securities.

Neither the U.S. Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Share |

Total | |||||||

| Public offering price |

$ | 7.25 | $ | 47,999,974 | ||||

| Underwriting discounts and commissions(1) |

$ | 0.47 | $ | 3,032,309 | ||||

| Proceeds to the company, before expenses |

$ | 6.79 | $ | 44,967,665 | ||||

| (1) | Excluding 168,965 shares sold to members of our executive management at the public offering price for which the underwriter will not receive any discount and commissions. See “Underwriting (Conflicts of Interest)” for additional information about underwriting compensation. |

We have granted the underwriter the option for a period of up to 30 days to purchase up to an additional 993,102 shares.

As part of this offering, certain members of our executive management have agreed to purchase a total of 168,965 Class A common shares at the public offering price resulting in a gross proceeds of $1,224,996. The underwriter will not receive any discount and commissions on the sale of such shares.

The underwriters expect to deliver the Class A common shares to purchasers on or about October 1, 2019.

B. Riley FBR

The date of this prospectus is September 26, 2019

Table of Contents

| 1 | ||||

| 16 | ||||

| 16 | ||||

| 17 | ||||

| 18 | ||||

| 22 | ||||

| 23 | ||||

| 26 | ||||

| 27 | ||||

| 28 | ||||

| 29 | ||||

| 30 | ||||

| THE INTERNATIONAL CONTAINER SHIPPING AND CONTAINERSHIP LEASING INDUSTRY |

33 | |||

| 66 | ||||

| 76 | ||||

| 79 | ||||

| SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT |

83 | |||

| 85 | ||||

| 88 | ||||

| 97 | ||||

| 104 | ||||

| 105 | ||||

| 105 | ||||

| 105 | ||||

| 107 |

You should rely only on the information contained in this prospectus or in any free writing prospectus we may authorize to be delivered to you. We have not, and the underwriters have not, authorized any other person to provide you with additional, different or inconsistent information. If anyone provides you with additional, different or inconsistent information, you should not rely on it. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission, (the “SEC” or “Commission”), is effective. We are not, and the underwriters are not, making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should not assume that the information appearing in this prospectus is accurate as of any date other than the date on the front cover of this prospectus unless otherwise specified herein. Our business, financial condition, results of operations and prospects may have changed since that date. Information contained on our website does not constitute part of this prospectus.

We have not taken any action to permit a public offering of these securities outside the United States or to permit the possession or distribution of this prospectus outside the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about and observe any restrictions relating to the offering of these securities and the distribution of this prospectus outside the United States.

Table of Contents

This summary highlights certain of the information that appears later in this prospectus or in other documents incorporated by reference in this prospectus. This summary may not contain all of the information that may be important to you. As an investor, you should carefully review the entire prospectus, including the section of this prospectus entitled “Risk Factors” and the more detailed information that appears later in this prospectus or is contained in the documents that we incorporate by reference in this prospectus before making an investment in our Class A common shares. The information presented in this prospectus assumes, unless otherwise indicated, that the underwriters’ option to purchase additional Class A common shares is not exercised.

Unless the context otherwise requires, references to the “Company,” “we,” “us,” “our” or “Global Ship Lease” refer to Global Ship Lease, Inc., “CMA CGM” refers to CMA CGM S.A., currently our principal charterer, “Poseidon Containers” refers to Poseidon Containers Holdings LLC and K&T Marine LLC, collectively, with whom we completed a strategic combination on November 15, 2018, Technomar Shipping Inc. (“Technomar”) refers to our ship technical manager (“Technical Manager”), ConChart Commercial Inc. (“Conchart”) refers to our commercial ship manager (“Commercial Manager”, and together with Technomar the “Managers”), and “MSI” refers to Maritime Strategies International Limited, our industry expert. Unless otherwise indicated, all references to “$” and “dollars” in this prospectus are to U.S. dollars. We use the term “TEU”, meaning twenty-foot equivalent unit, the international standard measure of container size, in describing volumes in world container trade and other measures, including the capacity of our containerships, which we also refer to as ships. Unless otherwise indicated, we calculate the average age of our ships on a weighted average basis, based on TEU capacity. References to our 2018 Annual Report refer to our Annual Report on Form 20-F for the fiscal year ended December 31, 2018, that was filed with the SEC on March 29, 2019, which is incorporated herein by reference.

On March 25, 2019, we effected a one-for-eight reverse stock split of our Class A common shares. All share and per share amounts disclosed in this prospectus have been retroactively adjusted to reflect the reverse stock split.

Our Company

Global Ship Lease, Inc. is a Republic of the Marshall Islands corporation that owns a fleet of mid-sized and smaller containerships which are chartered out under fixed-rate charters to reputable container shipping companies (“liner companies” or “liner operators”).

We were formed in 2007 to purchase and charter back 17 containerships owned or to be purchased by CMA CGM, then the third largest containership operator in the world by number of ships.

On November 15, 2018, we completed a transformative transaction and acquired Poseidon Containers’ 20 containerships, one of which, the Argos, was contracted to be sold, which sale was completed in December 2018, which we refer to herein as the “Poseidon Transaction”. References herein to the “GSL Fleet” are to the 19 ships that were owned by us prior to the consummation of the Poseidon Transaction, and references to the “Poseidon Fleet” are to the 19 ships that we acquired as a result of the Poseidon Transaction, excluding the Argos. On the closing of the Poseidon Transaction, we issued to the Poseidon unitholders 3,005,603 Class A common shares and 250,000 Series C Preferred Shares, which are convertible to an aggregate of 12,955,187 Class A common shares in certain circumstances, and assumed the debt of Poseidon Containers, which amounted to $509.7 million as of November 15, 2018.

1

Table of Contents

Following the announcement of the Poseidon Transaction on October 29, 2018, we have agreed multiple new charters in an improving market over multi-year durations, to renew or replace expiring charters, that have resulted in material improvements to key performance metrics, such as:

| • | Increased remaining contract duration: Since the announcement of the Poseidon Transaction, we have agreed to 27 new charters with an aggregate contract duration of 68 years, resulting in TEU-weighted average remaining contract duration for our entire fleet, as of June 30, 2019 and including subsequent announcements of new charters and options to extend which are under our control, and assuming the mid-point of the redelivery period, of 2.9 years, or 3.3 years also including options to extend which are under the charterers’ control and assuming the latest redelivery date. The charter-attached value of our fleet of 41 vessels as at June 30, 2019 was $1.34 billion. |

| • | Significant new contracted revenue: Since announcing the Poseidon Transaction, we have entered into charters, both as charter renewals and for ship acquisitions, which are expected to generate $511.9 million contracted revenue (measured over the term of the charter to the mid-point of redelivery including options to extend these new charters which are under our control). Contracted future revenue was $835.4 million, as of June 30, 2019 and including subsequent agreements of new charters (assuming the mid-point of redelivery under charters and including options to extend which are under our control). We estimate that our contracted revenue represents 99% of Adjusted EBITDA for 2019, 89% for 2020 and 76% for 2021 on the assumption that ships coming off charter are re-employed at 10 year historical average rates, less 5% commissions. |

In addition, in May 2019, we agreed to acquire three 2004-built 7,849 TEU containerships. Shortly after delivery in May 2019, the first ship, GSL Eleni, commenced a five-year charter with Maersk Line. The second ship, GSL Grania, was delivered in September 2019 and commenced a three-year charter with Maersk Line, with two consecutive one-year extensions at the charterer’s option. The remaining ship, GSL Kalliopi, is expected to be delivered in late September or early October 2019 and upon delivery is scheduled to commence a three-year charter with Maersk Line, with two consecutive one-year extensions at the charterer’s option.

As of the date of this prospectus, we owned 40 containerships and have agreed to acquire one further ship. Following the delivery of this ship, we will own 41 mid-sized and smaller containerships of which nine (representing 31% of our fleet by TEU capacity) are new-design, high-specification, fuel-efficient, and wide-beam. Our fleet, pro forma for the delivery of the remaining vessel we have agreed to acquire, has a total capacity of 224,162 TEU, making us the 13th largest non-operating owner of containerships as of June 30, 2019, according to MSI. Our fleet’s average size is 5,467 TEU, with a TEU weighted average age of 11.9 years.

All of our ships are chartered out on time charters, representing contracted future revenue of $835.4 million as of June 30, 2019, including subsequent new charters and options to extend which are under our control, and assuming the mid-point of redelivery, over a TEU-weighted average remaining term of 2.9 years. Contracted future revenue was $916.4 million on the same basis, but also including options to extend which are under the charterers’ control and assuming the latest redelivery date, over a TEU-weighted average remaining term of 3.3 years. By applying the Adjusted EBITDA Margin of 62.2% for the six months ended June 30, 2019 to contracted future revenue, this would imply Contracted Adjusted EBITDA of $519.6 million on our contracted future revenue of $835.4 million (to the mid-point of redelivery and including options to extend charters which are under our control) and $570.0 million on our future contracted revenue of $916.4 million (also including options to extend which are under the charterers’ control and assuming the latest redelivery). Adjusted EBITDA, Adjusted EBITDA Margin and Contracted Adjusted EBITDA are non-U.S. GAAP measures. For a description of Adjusted EBITDA, Adjusted EBITDA Margin and Contracted Adjusted EBITDA and a reconciliation of these measures to net income, the most directly comparable US GAAP financial measure, please see “Summary Financial Data—Non-U.S. GAAP Financial Measures” below.

2

Table of Contents

On January 2, 2019, as a consequence of the completion of the Poseidon Transaction, all of our issued and outstanding Class B common shares converted one-for-one into Class A common shares. On March 25, 2019, we effected a one-for-eight reverse stock split of our Class A common shares, which our shareholders authorized at our special meeting of shareholders held on March 20, 2019. There was no change to the trading symbol, number of authorized shares, or par value of our Class A common shares in connection with the reverse stock split. As of June 30, 2019, there were 9,942,950 Class A common shares issued and outstanding, along with 250,000 Series C Preferred Shares, which are convertible into 12,955,187 Class A common shares in certain circumstances. All share and per share amounts disclosed in this prospectus give effect to the reverse stock split retroactively, for all periods presented.

The mailing address of our principal executive office is c/o Global Ship Lease Services Limited, 25 Wilton Road, London SW1V 1LW, United Kingdom, and our telephone number is +44 (0) 20 3998 0063. Our website address is www.globalshiplease.com. The information included on our website is not incorporated herein by reference. From time to time, we may use our website and social media outlets as channels of distribution of material company information.

Industry Overview

The following is a summary of certain industry information provided by Maritime Strategies International Ltd. (“MSI”), which appears later in this prospectus under the heading “The International Container Shipping and Containership Leasing Industry.”

Containerization is the most convenient and cost-effective way to transport a wide range of cargoes, predominantly a diverse selection of consumer, manufactured, and semi-manufactured goods. Furthermore, emissions per ton-mile of cargo carried compare favorably to other existing modes of transport.

The first containerized cargoes were shipped in the mid-1950s; global containerized trade volumes for 2018 are estimated to be 208 million TEU. As at June 30, 2019, the global containership fleet stood at 5,165 ships, with an aggregate capacity of 22.3 million TEU; 54.0% of this capacity is provided to liner operators by containership owners like GSL.

Cargo volumes have grown every year since the industry’s inception – except 2009, during the Global Financial Crisis – with the growth in the containerized transport of refrigerated (“reefer”) cargo tending to outpace that of overall containerized trade. As at June 30, 2019, MSI forecasts that global containerized trade will grow by 2.8% in 2019 and 4.1% in 2020.

3

Table of Contents

Growth of Containerized Trade, Including 2019 and 2020 Forecasts

The containerized supply chain extends throughout the world. The Mainlane trades are those linking the major manufacturing economies in Asia with the major consumer economies in North America (Transpacific) and Europe (Asia-Europe), and the Transatlantic trade. However, over 70% of global containerized trade volumes are in the non-Mainlane trades, with intra-regional trades alone representing almost 39%. Indeed, the largest trade grouping – representing almost a third of global volumes – comprises the intra-Asian trades connecting that region’s rapidly growing markets. Non-Mainlane trades are predominantly served by mid-size and smaller containerships, like those in our fleet.

4

Table of Contents

Containership Deployment by Trade, as at June 30, 2019

The Transpacific trades represent 12.5% of overall volumes, while trade between China and the US (and vice-versa) represents 6.7% of global containerized volumes. One consequence of trade tensions between the US and China has been the increased market share of non-Chinese manufacturers on the Asia-US trade via a process of cargo substitution. Over the first six months of 2019, MSI estimates that US containerized imports from China and Hong Kong shrank by 5.3% (equal to a decrease of 290,000 TEU), while US imports from ASEAN countries grew by 23.0% (equal to an increase of 295,000 TEU), and imports from Japan, South Korea and Taiwan grew by 8.9% (equal to an increase of 93,000 TEU). We believe cargo substitution may stimulate additional demand for mid-size and smaller vessels in the intra-Asian trades.

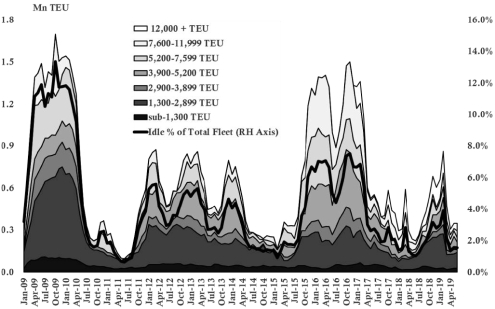

The container shipping industry is both cyclical and seasonal. We believe that supply / demand fundamentals are currently strongly supportive, particularly for the mid-size and smaller ship sizes upon which GSL is focused. As of June 30, 2019, MSI estimates that idle capacity for the global fleet was only 1.5%, capacity scrapped during the first half of 2019 exceeded capacity scrapped in full year 2018, and the newbuilding orderbook – which is scheduled to deliver over the next two to three years – was limited, with an orderbook-to-fleet ratio of 11.2% (down from a peak of over 60% in 2007). For ships of 2,000 – 9,999 TEU (mid-size and smaller) the ratio was 2.6%, with no ships on order between 4,000 and 9,999 TEU – sizes representing over 80% of GSL fleet capacity. As of June 30, 2019, MSI estimates that the lead time from order to delivery of a new ship would be approximately two years.

5

Table of Contents

Estimated Capacity on Order by Segment, as at June 30, 2019

A combination of scrapping and under-investment in the sector has led to minimal, and in some cases net-negative, fleet growth in the mid-size and smaller ship fleet segments in recent years. As a result, these size segments are comparatively older than those for very large containerships, where recent investment has tended to be focused. Furthermore, we believe that consolidation and bankruptcies in the shipyard sector (MSI estimates that the number of active shipyards has decreased by 65% since 2007), together with a more coordinated approach from the liner operator alliances, is improving ordering discipline and reducing the risk of supply-side overshoot going forward.

6

Table of Contents

Net Fleet Growth by Segment, 2016 through June 30, 2019

We expect the implementation of industry-wide regulatory changes on emission controls starting January 1, 2020 (“IMO 2020”), which are expected to increase the unit cost of fuel due to the anticipated price premium of low Sulphur fuel, to further improve industry fundamentals as, among other things, operators reduce operating speeds as a cost control measure to reduce fuel consumption, thereby decreasing the effective supply of containerships. As at June 30, 2019, MSI estimates that slowing the global fleet by one knot would imply a reduction in effective supply of 6.7%.

IMO 2020 is also expected to increase the commercial appeal of fuel-efficient vessels which allow liner operators to reduce their operating costs per TEU of cargo carried (“slot costs”). The greater the cargo carrying capacity and fuel efficiency of a ship, the lower the slot costs. Latest generation “Eco” ships are significantly more fuel efficient than their pre-Eco peers, enhancing their earnings in the charter market. However, for mid-size and smaller ships, pre-Eco specification vessels are still the standard: as at June 30, 2019, MSI estimates that pre-Eco ships represented between 77% and 91% of capacity for the size segments below 7,500 TEU, and 58% for the 7,500 – 9,999 TEU segment.

We believe that firming rates in the charter market, particularly for larger mid-size (Post Panamax) ships, evidence strengthening industry fundamentals. An additional positive catalyst is ships being taken out of service for retro-fitting with exhaust gas scrubbers (an alternate means of complying with IMO 2020). MSI estimates that 1.1% of the global containership fleet (by number of vessels) had been scrubber-fitted by June 30, 2019, and forecasts that around 15.0% of containerships will ultimately be fitted with exhaust gas cleaning technology.

Charter rates for 6,500 TEU and 8,500 TEU ships have more than doubled since the end of 2018.

7

Table of Contents

Asset Value and Spot Market Time Charter Rate Development, September 1, 2016 through June 30, 2019

Panamax and Post-Panamax Time charter Earnings Developments since Q4 2018

8

Table of Contents

We believe that the fuel-efficient, low slot characteristics of our ships will allow us to capitalize on the trends described above, enhancing the earnings capacity and value of the GSL fleet over time.

Our Competitive Strengths.

We believe that we possess a number of competitive strengths that differentiate us and will allow us to capitalize on opportunities in the containership sector, including:

Experienced Management Team. Members of our management team, board of directors and Managers have extensive experience in the container shipping industry and have long-term relationships with companies, individuals and institutions within the wider shipping industry. Our Executive Chairman, George Giouroukos, has more than 25 years of leadership and shipping industry experience, while our Chief Executive Officer, Ian Webber, has 30 years of shipping industry experience, 12 of which serving as our Chief Executive Officer. We believe that we will be able to capitalize on the experience and relationships of our management, board of directors and Managers to identify future acquisitions and charter opportunities beyond those widely and publicly marketed, expand our customer base, and finance these acquisitions and refinance our debt. See “Item 6. Directors, Senior Management and Employees” in our 2018 Annual Report, which is incorporated herein by reference.

Significant Contracted Revenue. All of our ships are chartered out on time charters, representing contracted future revenue of $835.4 million as of June 30, 2019, including subsequent new charters and options to extend which are under our control, and assuming the mid-point of redelivery, over a TEU-weighted average remaining term of 2.9 years. Contracted future revenue was $916.4 million on the same basis, but also including options to extend which are under the charterers’ control and assuming the latest redelivery date, over a TEU-weighted average remaining term of 3.3 years. Our contracted revenue mostly consists of revenue generated by our larger ships as these have higher daily charter rates and longer charter durations provides substantial forward visibility on earnings. Our smaller, lower-earning ships are mostly employed on shorter term contracts, which we believe will provide upside earnings potential in what we anticipate will be a firming charter market after a protracted downturn. Since announcing the Poseidon Transaction, we have entered into charters, both as charter renewals and for ship acquisitions, which are expected to generate $511.9 million contracted revenue (measured over the term of the charter to the mid-point of redelivery including options to extend these new charters which are under our control).

Diversified Portfolio of Charterers. As of June 30, 2019, charterers of our ships included Maersk Line, MSC, COSCO-OOCL, CMA CGM, Hapag-Lloyd and ZIM. In addition, our Commercial Manager has established relationships with, and has previously arranged charters with, many other reputable liner operators, such as ONE, Wan Hai, Evergreen and Seaboard Marine. We expect to continue to capitalize on our senior management’s and Commercial Manager’s long-standing relationships with leading liner companies. We believe that the experience of our senior management team, coupled with our Technical Manager’s extensive experience and reputation, will continue to assist us in securing high employment coverage for our ships to facilitate our future growth.

Focused Fleet Composition. Our fleet is focused on high specification, mid-sized and smaller ships, which we believe are undersupplied in the market and have multiple deployment opportunities. We own and operate 41 containerships, including the ship that will be delivered to us in late September or early October 2019, ranging in size between 2,207 TEU and 11,040 TEU, built at reputable shipyards, with high specifications, and which are well-maintained. Such mid-size and smaller ships are operationally flexible and are core to servicing multiple non-arterial, intermediate, and intra-regional container trades which, in aggregate, represented over 70% of global containerized trade volumes in 2018. Limited investment by the industry in recent years in mid-sized and smaller containerships has resulted in a small orderbook to be delivered over the next two-three years (the

9

Table of Contents

orderbook to fleet ratio for 2,000—10,000 TEU ships was 2.6% as of June 30, 2019, versus an overall ratio of 11.2%) and an aging global fleet, with limited availability of latest-generation ships in these segments.

Fleet with High Technical Specifications. Value-adding attributes that render our ships attractive to our customers, the liner operators, include capacity to carry a large number of temperature-controlled containers (“reefers”), wide-beam and fuel-efficient designs, and onboard cranes (“gear”) for cargo handling. We believe that these features enable our fleet to achieve higher levels of employment and earnings against ships with lower specifications. 72% of our fleet capacity is made up of Post-Panamax containerships larger than 5,500 TEU, which provide enhanced ship stability and thus greater cargo carrying capacity. Cargo carrying capacity is an important selection criterion for liner operators as it reduces slot cost, which is calculated for any given ship as daily fuel cost plus daily charter hire divided by standardized loadable capacity. Nine of our Post-Panamax ships are also latest-generation, fuel efficient “Eco” ships, which further enhance slot cost economics for liner operators and command an earnings premium in the charter market versus non-Eco ships and have the potential to provide longer term charters. Fuel efficiency becomes even more valuable as fuel prices rise, as is anticipated with the introduction of industry-wide emission control regulations from January 2020 (“IMO 2020”), with which the vast majority of ships will comply by burning higher cost, low sulfur fuel. Furthermore, we believe there is a clear correlation between low slot costs and low emissions per TEU, favoring our low slow cost fleet.

Capitalize on Cascade. The shipping industry up-sizes ships over time in order to capture economies of scale by increasing the carrying capacity of ships. This up-sizing is also referred to as the “cascade,” and involves larger ships progressively displacing smaller ships into other trade lanes. Non-mainlane, intermediate, and intra-regional trades are of fundamental importance to global containerized trade—representing, in aggregate, over 70% of global containerized trade volumes in 2018—and are predominantly served by mid-size and smaller ships, which we believe are supply-constrained. We also believe that our fuel-efficient, low slot cost ships position us to capitalize on cascading opportunities in these markets. As of June 30, 2019, according to MSI, 42.0% of the global fleet (by number of ships) was comprised of ships of 2,000 TEU or smaller, providing significant cascading opportunities for even the smallest ships in our fleet (2,200 TEU).

Efficient Ship Operations. We believe that our Technical Manager’s experience in the technical management of containerships, and their reputation in the shipping industry as operators with high safety and operating standards, are important in servicing our charterers, who depend on reliable ships and responsible containership owning companies to meet their exact and demanding ship scheduling requirements. Our Technical Manager has been managing ships successfully since 1994 and this depth of experience not only provides our customers with a high level of service quality and confidence but also gives us competitive average daily operating costs. Despite significant drydocking of our ships for regulatory surveys and upgrades, utilization for the six months ended June 30, 2019 was 96.9%. Utilization for the three months ended March 31, 2019, which was not affected by elevated levels of drydocking, was 99.8%. In addition, our Technical Manager has experience in upgrading ships, including reefer capacity and fuel efficiency and in the efficient design of scrubbers, all of which raise our ships to higher commercial standards enhancing their marketability and earning capacity.

Growth Track Record. We have a proven ability to grow by purchasing ships with pre-agreed charters that are immediately accretive to cashflow and earnings, while concurrently putting in place competitively-priced and conservatively-structured debt to facilitate such growth. Our Executive Chairman, George Giouroukos, has structured and concluded over 250 secondhand and newbuilding ship transactions. The strategic combination between GSL and Poseidon Containers in November 2018 also demonstrates our capacity to successfully execute transformative corporate transactions. We believe that our senior management team’s extensive knowledge of, and contacts within, the container shipping industry will allow us to continue to add value-accretive ships and charters to our portfolio.

10

Table of Contents

Multiple Financing Sources. Access to cost-effective capital is important in the container shipping industry. As a publicly listed company with a business model primarily oriented towards providing medium-term charters to reputable counterparties, we can potentially access equity and debt markets, both private and public, on a recurrent basis. In a capital-constrained environment, we believe that being a publicly listed company with a high level of transparency and reporting is an advantage in competing with other containership owning companies, which are predominantly private and do not have access to such diverse sources of capital. In addition, our management team has extensive and long-standing relationships with commercial banks that provide us with access to the traditional secured loan bank market. Specifically, since the Poseidon Transaction, our significantly expanded banking relationships now include Citi, Credit Agricole, Deutsche Bank, ABN Amro, DVB, CIT, Entrust, ATB, Hellenic Bank and Siemens, most of which participated in our new syndicated $268.0 million senior secured credit facility.

Our Business Strategies

Our primary objective is to maximize value for our shareholders by pursuing the following strategies:

Maintain Fleet Focus. We intend to maintain our focus on containerships of 2,000 – 11,000 TEU, weighted towards wide-beam, high-reefer, fuel-efficient ships of 5,500 – 10,000 TEU. We believe the cost-return characteristics of ships in this size segment are attractive. Specifically, they are sought after by charterers given their operational flexibility and low slot costs and should thereby allow us to manage our fleet deployment effectively, locking in upside earnings potential for shareholders by securing longer-term charters generating contracted cashflows. Furthermore, due to scarce capital being disproportionately allocated to the construction of the largest containerships for the main East-West trades lanes, such as Asia – Europe, the order-book for containerships below 10,000 TEU is at historically low levels and, according to MSI, there are no ships on order in our area of focus, the 4,000 TEU and 9,999 TEU segment, which, combined with reasonable demand growth for container shipping services, particularly in the trade lanes where our ships are best deployed, is expected to result in continuing improvements in charter rates and hence asset values, over time. We expect supply to tighten further for these ship segments with the implementation on January 1, 2020 of the new industry-wide emission controls under IMO 2020, which we believe may prompt liner operators to slow down their ships in order to reduce fuel burn and thus cost, reducing effective supply.

Optimize Charter Portfolio. We intend to proactively manage our portfolio of charters to lock in upside earning potential, while also providing downside protection through charter cover. This provides significant forward visibility of stable cashflows, while preserving the flexibility to capitalize on potentially rising charter rates. We currently charter most of our high revenue producing ships under medium term time charters of between three to five years, with staggered maturities, while the remainder of the fleet, mostly our smaller ships, are on shorter term charters of less than 12 months to position us to benefit from market increases in charter rates. Additionally, we will continue to charter our ships to reputable charterers, such as our long-standing clients Maersk Line, MSC, COSCO-OOCL, CMA CGM, Hapag Lloyd and ZIM, and will continue to expand the number of leading liner companies chartering our ships in order to further diversify our portfolio of charters from customer, geographic and maturity perspectives.

Moderate Leverage Level and Reduced Cost of Debt. Our mandatory debt repayment profile will result in substantial debt reduction over the next few years. We believe that reducing our leverage and maintaining debt at a moderate level will enable us to reduce our overall cost of debt, enhance our financial flexibility and allow us to make opportunistic acquisitions consistent with our strategy. We expect to finance future ship acquisitions, with cash on hand, borrowings under new credit facilities, or subject to favorable market conditions, public debt or equity offerings, or a combination thereof.

Implement Disciplined Growth. We intend to continue to grow and renew our fleet mainly by acquiring second-hand containerships with high specifications and fuel efficiency, that are already employed on charters or

11

Table of Contents

that can be so employed immediately following their acquisition, as market conditions allow. When evaluating these future acquisitions, we will consider, among other things, fundamental developments in the container shipping industry, the value of the ship compared to historical levels, the cash flow expected to be earned by the ship in relation to its value, the credit quality of the charterer and duration and terms of charter contracts, its condition and technical specifications, as well as the overall diversification of our fleet and customer portfolio. We believe that attractive, counter-cyclical investment opportunities are available in the market. These may include both structured sale and leaseback transactions with liner companies and the acquisition of selected, attractively-priced ships, in the sale and purchase market. In addition, we will evaluate and consider strategic corporate acquisitions on a selective and prudent basis.

Leverage Our Managers’ Experience. We intend to leverage our Technical Manager’s expertise to continue to manage our ships efficiently and reliably at a low daily operating cost, as well as support future growth. We believe that our Technical Manager is able to oversee the technical management of our fleet at a cost than is lower than we could achieve in-house and which is competitive compared to other independent ship management companies. Additionally, we believe that our outsourced management arrangements provide scalability to facilitate growth without the incurrence of significant additional overheads. In addition, our Technical Manager has experience in upgrading the reefer capacity and fuel efficiency of ships, and in the efficient design of scrubbers, as well as other characteristics that raise our ships to higher commercial standards enhancing their marketability and earning capacity. Moreover, our Commercial Manager has direct relationships with liner companies as evidenced by multiple long-term contracts, including repeat business, secured since the completion of the Poseidon Transaction.

12

Table of Contents

Our Fleet

The table below provides information about our fleet of 41 containerships as of September 16, 2019:

| Ship Name | Capacity in TEUs |

Lightweight (tons) |

Year Built |

Charterer | Earliest Charter |

Latest Charter |

Daily Charter Rate $ |

|||||||||||||||||||

| CMA CGM Thalassa |

11,040 | 38,577 | 2008 | CMA CGM | 4Q25 | 1Q26 | 47,200 | |||||||||||||||||||

| UASC Al Khor(1) |

9,115 | 31,764 | 2015 | Hapag-Lloyd | 1Q22 | 2Q22 | 34,000 | |||||||||||||||||||

| Anthea Y(1) |

9,115 | 31,890 | 2015 | COSCO | 2Q20 | 3Q20 | 39,200 | |||||||||||||||||||

| Maira XL(1) |

9,115 | 31,820 | 2015 | COSCO | 2Q20 | 3Q20 | 39,200 | |||||||||||||||||||

| MSC Tianjin |

8,667 | 34,243 | 2005 | MSC | 2Q24 | 3Q24 | (2) | — | (2) | |||||||||||||||||

| MSC Qingdao |

8,667 | 34,305 | 2004 | MSC | 2Q24 | 3Q24 | (2) | — | (2) | |||||||||||||||||

| GSL Ningbo |

8,667 | 34,243 | 2004 | Maersk | 3Q20 | 3Q20 | 12,400 | (3) | ||||||||||||||||||

| GSL Kalliopi |

7,849 | 29,245 | 2004 | Maersk | 3Q22 | 4Q24 | (4) | — | (4) | |||||||||||||||||

| GSL Grania |

7,849 | 29,261 | 2004 | Maersk | 3Q22 | 4Q24 | (4) | — | (4) | |||||||||||||||||

| GSL Eleni |

7,849 | 29,261 | 2004 | Maersk | 2Q24 | 3Q24 | (4) | — | (4) | |||||||||||||||||

| Mary(1) |

6,927 | 23,424 | 2013 | CMA CGM | 3Q23 | 4Q23 | 25,910 | |||||||||||||||||||

| Kristina(1) |

6,927 | 23,424 | 2013 | CMA CGM | 2Q24 | 3Q24 | 25,910 | |||||||||||||||||||

| Katherine(1) |

6,927 | 23,424 | 2013 | CMA CGM | 1Q24 | 2Q24 | 25,910 | |||||||||||||||||||

| Alexandra(1) |

6,927 | 23,424 | 2013 | CMA CGM | 1Q24 | 2Q24 | 25,910 | |||||||||||||||||||

| Alexis(1) |

6,882 | 23,919 | 2015 | CMA CGM | 1Q24 | 2Q24 | 25,910 | |||||||||||||||||||

| Olivia I(1) |

6,882 | 23,864 | 2015 | CMA CGM | 1Q24 | 2Q24 | 25,910 | |||||||||||||||||||

| CMA CGM Berlioz |

6,621 | 26,776 | 2001 | CMA CGM | 2Q21 | 4Q21 | 34,000 | |||||||||||||||||||

| Agios Dimitrios |

6,572 | 24,746 | 2011 | MSC | 3Q19 | 4Q23 | 12,500 | (5) | ||||||||||||||||||

| Tasman |

5,936 | 25,010 | 2000 | ZIM | 3Q19 | 3Q19 | (6) | 11,500 | (6) | |||||||||||||||||

| Dimitris Y |

5,936 | 25,010 | 2000 | ZIM | 3Q19 | 3Q19 | (7) | 16,750 | (7) | |||||||||||||||||

| Ian H |

5,936 | 25,128 | 2000 | ZIM | 1Q21 | 2Q21 | 14,500 | |||||||||||||||||||

| Dolphin II |

5,095 | 20,596 | 2007 | HMM | 3Q19 | (8) | 4Q19 | (8) | 7,700 | (8) | ||||||||||||||||

| Orca I |

5,095 | 20,696 | 2006 | Maersk | 2Q20 | (9) | 2Q21 | (9) | 9,000 | (9) | ||||||||||||||||

| CMA CGM Alcazar |

5,089 | 20,087 | 2007 | CMA CGM | 4Q20 | 2Q21 | 33,750 | |||||||||||||||||||

| CMA CGM Château d’If |

5,089 | 20,100 | 2007 | CMA CGM | 4Q20 | 2Q21 | 33,750 | |||||||||||||||||||

| CMA CGM Jamaica |

4,298 | 17,272 | 2006 | CMA CGM | 3Q22 | 1Q23 | 25,350 | |||||||||||||||||||

| CMA CGM Sambhar |

4,045 | 17,355 | 2006 | CMA CGM | 3Q22 | 1Q23 | 25,350 | |||||||||||||||||||

| CMA CGM America |

4,045 | 17,355 | 2006 | CMA CGM | 3Q22 | 1Q23 | 25,350 | |||||||||||||||||||

| GSL Valerie |

2,824 | 11,971 | 2005 | MSC | 2Q20 | 3Q20 | 9,000 | |||||||||||||||||||

| Athena |

2,762 | 13,538 | 2003 | MSC | 1Q20 | 2Q20 | 9,000 | |||||||||||||||||||

| Maira |

2,506 | 11,453 | 2000 | MSC | 3Q19 | 3Q19 | 8,500 | (10) | ||||||||||||||||||

| Nikolas |

2,506 | 11,370 | 2000 | MSC | 1Q20 | 1Q20 | 9,000 | |||||||||||||||||||

| Newyorker |

2,506 | 11,463 | 2001 | MSC | 1Q20 | 1Q20 | 9,000 | |||||||||||||||||||

| CMA CGM La Tour |

2,272 | 11,742 | 2001 | CMA CGM | 4Q19 | 4Q19 | 15,300 | |||||||||||||||||||

| CMA CGM Manet |

2,272 | 11,742 | 2001 | CMA CGM | 4Q19 | 4Q19 | 15,300 | |||||||||||||||||||

| CMA CGM Matisse |

2,262 | 11,676 | 1999 | CMA CGM | 4Q19 | 4Q19 | 15,300 | |||||||||||||||||||

| CMA CGM Utrillo |

2,262 | 11,676 | 1999 | CMA CGM | 3Q19 | 3Q19 | 15,300 | (11) | ||||||||||||||||||

| GSL Keta |

2,207 | 11,731 | 2003 | ANL | 3Q19 | 3Q19 | 8,450 | (12) | ||||||||||||||||||

| GSL Julie |

2,207 | 11,731 | 2002 | CMA CGM | 3Q19 | 4Q19 | 7,200 | (13) | ||||||||||||||||||

| Kumasi |

2,207 | 11,731 | 2002 | CMA CGM | 4Q19 | 1Q21 | (14) | 9,800 | (14) | |||||||||||||||||

| Marie Delmas |

2,207 | 11,731 | 2002 | CMA CGM | 4Q19 | 1Q21 | (14) | 9,800 | (14) | |||||||||||||||||

| (1) | Modern design, high reefer capacity fuel efficient ships. |

| (2) | Five year charter to MSC at implied Adjusted EBITDA of $25.6 million per ship for the period. |

| (3) | Charterer has exercised its option to extend by 12 months from September 21, 2019 at $18,000 per day. |

13

Table of Contents

| (4) | GSL Eleni delivered in May 2019; GSL Grania delivered in September 2019 and GSL Kalliopi is scheduled to be delivered in late September or early October 2019. GSL Eleni chartered for five years; GSL Grania and GSL Kalliopi are or will be chartered for three years plus two successive periods of one year at option of the charterer. Implied Aggregate Adjusted EBITDA of $32.0 million for firm periods, increasing to $47.0 million if all options are exercised. |

| (5) | Thereafter, we have the option, callable in 4Q19, to extend for four years at $20,000 per day. |

| (6) | Thereafter, a new charter with Maersk Line for 30 – 38 months at an implied Adjusted EBITDA of $5.3 million for the median period. Additional 12 – month extension at charterer’s option, for an additional $4.4 million implied Adjusted EBITDA. |

| (7) | Thereafter in direct continuation, 21-24 months to ZIM at $14,500 per day. |

| (8) | Rate increases to $11,500 per day from August 14, 2019. |

| (9) | Rate increases to $10,000 per day from June 3, 2020. |

| (10) | Thereafter, 6-7 months to MSC at $8,250 per day. |

| (11) | Thereafter, 6-7 months to CMA CGM at $8,500 per day. |

| (12) | Thereafter 50 – 90 days to OOCL at $8,700 per day. |

| (13) | $ 7,200 per day between August 16, 2019 and October 16, 2019, at charterer’s option, with an option in favor of charterer to extend from October 16, 2019 at $8,500 per day for six months plus or minus 30 days. |

| (14) | We have the option to extend to December 31, 2020 plus or minus 90 days, at $9,800 per day. |

Employment of Our Fleet

We employ the ships in our fleet on time charters. A time charter is a contract for the use of a ship for a fixed period of time at a specified daily rate. Under a time charter, the ship owner provides and bears the cost of crew, lubricating oil and all maintenance and other services related to the ship’s operation, the cost of which is recovered from the daily charter rate. We are also responsible for insuring our interests in the ship and liabilities as owner arising from its use. The charterer is responsible for substantially all of the ship’s voyage costs, such as fuel (bunker) costs, canal fees, port expenses, cargo handling costs and extra war risk insurance costs if the ship is deployed outside normal insurance limits and enters areas which are specified by the insurance underwriters as being subject to additional premiums.

The term for a time charter commences on the ship’s delivery to the charterer. Time charter agreements may include options, in favor of the owner or the charterer, to extend the charter on pre-agreed terms. Charters may be extended on mutually agreed terms, or the ship may be re-delivered by the charterer at the end of the charter period, within a pre-agreed time window (to allow for operational flexibility), in which case we would seek alternate employment with another charterer.

Our charters are with a number of different charterers and expire on different dates over a period of time. We believe the diversified charterer base reduces counterparty risk and the staggered expirations of our charters reduces our exposure to re-chartering risk and may mitigate the impact of the cyclical nature of the container shipping industry.

Management of our Ships

Technomar provides day-to-day technical ship management services for all of our ships.

Global Ship Lease Services Limited (“GSLS”), our wholly owned subsidiary, is the commercial manager for 18 of our ships. It has entered into a Commercial Advisory Services and Exclusive Brokerage Services Agreement (“EBSA”) with Conchart, whereby Conchart is appointed to provide commercial advisory and exclusive brokerage services. The remaining 23 ships in our fleet are or will be subject to a commercial management agreement directly with Conchart, on terms substantially similar to those of the EBSA.

14

Table of Contents

For more information regarding management of our ships, please see “Item 4. Information on the Company-B. Business Overview-Ship Management” in our 2018 Annual Report, which is incorporated herein by reference.

Risk Factors

We face a number of risks associated with our business and shipping industry and must overcome a variety of challenges to utilize our strengths and implement our business strategies. These risks relate to, among others, changes in the shipping industry, including supply and demand, charter rates, ship values, a downturn in the global economy, operational hazards inherent in container shipping industry and operations resulting in liability for damage to or destruction of property and equipment, pollution or environmental damage, inability to comply with covenants in our current indebtedness and borrowings we may enter into in the future, inability to finance capital projects, and inability to successfully employ our ships at the expiration of current charters.

You should carefully consider these risks, the risks described in “Risk Factors” and the other information in this prospectus and our most recent Annual Report on Form 20-F before deciding whether to invest in our Class A common shares.

Recent Developments

In May 2019, we agreed to acquire three 2004-built 7,849 TEU containerships. Shortly after delivery in May 2019, the first ship, GSL Eleni, commenced a five-year charter with Maersk Line. The second ship, GSL Grania, was delivered in September 2019 and commenced a three-year charter with Maersk Line, with two consecutive one-year extensions at the charterer’s option. The remaining ship, GSL Kalliopi, is expected to be delivered in late September or early October 2019 and is scheduled to commence a three-year charter with Maersk Line, with two consecutive one-year extensions at the charterer’s option.

In July 2019, GSL Keta, a 2003-built, 2,207 TEU containership, commenced a new charter with OOCL for minimum 50 days / maximum 90 days at a fixed rate of $8,700 per day. The charterer of GSL Ningbo, a 2004-built, 8,667 TEU containership, has exercised its option to extend the vessel’s charter for 12 months at a fixed rate of $18,000 per day starting from September 21, 2019.

At our 2019 Annual Meeting of Shareholders held on August 8, 2019, our shareholders approved the re-election of Messrs. Michael Chalkias and George Giouroukos, Term II Directors, to serve until our 2022 Annual Meeting of Shareholders, and ratified the appointment of PricewaterhouseCoopers S.A. as our independent public accounting firm for the fiscal year ending December 31, 2019.

In August 2019, Maersk exercised its option to extend the charter on GSL Ningbo by 12 months, commencing September 21, 2019, at an increased rate of $18,000 per day.

In August 2019, CMA CGM exercised its option to extend the charter on GSL Julie by six months, commencing October 16, 2019, at an increased rate of $8,500 per day and agreed to extend the charter of CMA CGM Utrillo by six-seven months, commencing September 16, 2019, at a rate of $8,500 per day.

In August 2019, MSC agreed to extend the charter of Maira by six-seven months, commencing September 17, 2019, at a rate of $8,250 per day.

In September 2019, we entered into a new syndicated $268.0 million senior secured credit facility comprised of two tranches (the “New Senior Loan”) with major commercial lenders Crédit Agricole, ABN AMRO, CIT, Hellenic Bank and Siemens. The first tranche of the New Senior Loan of $230.0 million was drawn

15

Table of Contents

down, in full, on September 23, 2019 and the proceeds will be used very shortly to refinance five of our existing senior credit facilities with maturities in December 2020 and April 2021 (the “First Tranche Refinancing”). As a result of the First Tranche Refinancing, three 2000-built 6,000 TEU ships, Tasman, Dimitris Y and Ian H, will become unencumbered. The second tranche of up to $38.0 million is available to us on similar terms until May 2020 to facilitate further refinancing. The final maturity date of the New Senior Loan is September 2024, five years after drawdown. Borrowings under the New Senior Loan bear interest at LIBOR plus a margin of 3.0% and the scheduled amortization is $5.2 million per quarter.

In September 2019, we also refinanced all of the existing indebtedness under our Junior Facility in the amount of $38.5 million (the “New Junior Facility”), with the only change being to extend its maturity from September 2023 to September 2024, consistent with the maturity date of the New Senior Loan. The other terms of the New Junior Facility remain consistent with the original Junior Facility, bearing interest at 10.0% and repayable in one balloon payment upon maturity.

In September 2019, we entered into an agreement with Kelso, whereby Kelso agreed to convert its outstanding Series C Preferred Shares into Class A common shares upon the repayment in full of our 9.875% First Priority Secured Notes due 2022.

We were incorporated in the Republic of the Marshall Islands on March 14, 2008 as GSL Holdings Inc.

On August 14, 2008, we merged with Marathon Acquisition Corp., a company then listed on The American Stock Exchange, and with the pre-existing Global Ship Lease, Inc., which was then wholly owned by CMA CGM. GSL Holdings, Inc. was the surviving entity, changed its name to Global Ship Lease, Inc. and became listed on The New York Stock Exchange (the “NYSE”).

The mailing address of our principal executive office is c/o Global Ship Lease Services Limited, 25 Wilton Road, London SW1V 1LW, United Kingdom, and our telephone number is +44 (0) 20 3998 0063.

We are incorporated under the laws of the Republic of the Marshall Islands, and as a consequence, you may encounter difficulty protecting your interests as shareholders, and your ability to protect your rights through the U.S. federal court system may be limited. Please refer to the sections entitled “Risk Factors” and “Enforcement of Civil Liabilities” for more information.

16

Table of Contents

| Class A Common shares offered |

6,620,686 Class A common shares. |

| Over-allotment |

We have granted the underwriter a 30-day option to purchase up to an additional 993,102 of our Class A common shares. |

| Class A Common shares outstanding immediately after the offering(1) |

16,563,636 Class A common shares. |

| 17,556,738 Class A common shares, if the underwriter exercises its option to purchase additional shares in full. |

| Use of proceeds |

We estimate that we will receive net proceeds of approximately $44.6 million from this offering assuming the underwriters’ over-allotment option is not exercised, and approximately $51.3 million if the underwriters’ option is exercised in full, in each case after deducting underwriting discounts and commissions and estimated expenses payable by us. |

| We intend to use the net proceeds of this offering for general corporate purposes, which may include, among other things, the acquisition of containerships in accordance with our growth strategy, or prepaying debt. However, we do not currently have definitive plans for any debt prepayments nor have we identified any potential acquisitions, and we can provide no assurance that we will be able to complete any debt prepayment or the acquisition of any vessel that we are able to identify. |

| Please read “Use of Proceeds.” |

| Listing |

Our Class A common shares are currently listed on the New York Stock Exchange under the symbol “GSL.” |

| Transfer agent |

Computershare Trust Company, N.A. |

| Risk factors |

Investment in our Class A common shares involves a high degree of risk. You should carefully read and consider the information set forth under the heading “Risk Factors” and all other information set forth in this prospectus before investing in our Class A common shares. |

| (1) | The number of Class A common shares outstanding immediately after the offering is based on Class A common shares outstanding as of September 26, 2019. |

17

Table of Contents

The following table sets forth summary consolidated financial and other data of the Company for the years ended December 31, 2018, 2017 and 2016 and as of December 31, 2018 and 2017 which is derived from our audited consolidated financial statements included in our annual report on Form 20-F for the year ended December 31, 2018, filed with the SEC on March 29, 2019, incorporated by reference herein. The summary consolidated financial and other data of the Company as of December 31, 2016, 2015 and 2014 and for the years ended December 31, 2015 and 2014, is derived from our audited consolidated financial statements not incorporated by reference herein but publicly available at www.sec.gov. The table also sets forth summary consolidated financial and other data of the Company as of June 30, 2019 and 2018 and for the six month periods ended June 30, 2019 and 2018 which is derived from our unaudited consolidated financial statements and the notes thereto, included in our Report on Form 6-K that was filed with the SEC on August 9, 2019, which is incorporated by reference herein.

The summary financial data set forth below should be read in conjunction with, and are qualified in their entirety by reference to, (i) our audited consolidated financial statements, including the related notes thereto, and “Item 5. Operating and Financial Review and Prospects,” as presented in our 2018 Annual Report, incorporated by reference herein, and (ii) our interim unaudited consolidated financial statements and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” as presented in our Report on Form 6-K, filed with the Commission on August 9, 2019, incorporated by reference herein. The summary historical financial information provided below does not purport to indicate results of operations as of any future date or for any future period.

CONSOLIDATED FINANCIAL DATA

| Six months ended June 30, |

Year ended December 31, | |||||||||||||||||||||||||||

| Summary Consolidated Statements of Income Data: | 2019 | 2018 | 2018 | 2017 | 2016 | 2015 | 2014 | |||||||||||||||||||||

| (Expressed in millions of U.S. dollars, except for per share data) | ||||||||||||||||||||||||||||

| Statements of Income |

||||||||||||||||||||||||||||

| Operating revenues: |

||||||||||||||||||||||||||||

| Time charter revenue |

$ | 127.6 | $ | 71.2 | $ | 157.1 | $ | 159.3 | $ | 166.8 | $ | 165.3 | $ | 138.7 | ||||||||||||||

| Operating expenses: |

||||||||||||||||||||||||||||

| Vessel operating expenses |

(41.8 | ) | (20.4 | ) | (49.3 | ) | (42.7 | ) | (45.4 | ) | (48.9 | ) | (47.6 | ) | ||||||||||||||

| Time charter and voyage expenses |

(3.6 | ) | (0.4 | ) | (1.6 | ) | (1.0 | ) | (0.7 | ) | (1.6 | ) | (1.3 | ) | ||||||||||||||

| Depreciation and amortization |

(21.7 | ) | (16.3 | ) | (35.5 | ) | (38.0 | ) | (42.8 | ) | (44.9 | ) | (41.1 | ) | ||||||||||||||

| Impairment of vessels |

— | — | (71.8 | ) | (87.6 | ) | (92.4 | ) | (44.7 | ) | — | |||||||||||||||||

| General and administrative expenses |

(4.1 | ) | (3.4 | ) | (9.2 | ) | (5.4 | ) | (6.2 | ) | (6.5 | ) | (7.0 | ) | ||||||||||||||

| Total operating expenses |

(71.2 | ) | (40.5 | ) | (167.4 | ) | (174.7 | ) | (187.5 | ) | (146.6 | ) | (97.0 | ) | ||||||||||||||

| Operating income (loss) |

56.4 | 30.7 | (10.3 | ) | (15.4 | ) | (20.7 | ) | 18.7 | 41.7 | ||||||||||||||||||

| Non-operating income (expense) |

||||||||||||||||||||||||||||

| Interest income |

0.8 | 0.6 | 1.4 | 0.5 | 0.2 | 0.1 | 0.1 | |||||||||||||||||||||

| Interest and other finance expenses |

(38.1 | ) | (21.5 | ) | (48.7 | ) | (59.4 | ) | (44.8 | ) | (48.2 | ) | (43.9 | ) | ||||||||||||||

| Gain on redemption of Series A Preferred Shares |

— | — | — | — | — | — | 8.6 | |||||||||||||||||||||

| Realized loss on interest rate derivative |

— | — | — | — | — | — | (2.8 | ) | ||||||||||||||||||||

| Unrealized gain on interest rate derivative |

— | — | — | — | — | — | 1.9 | |||||||||||||||||||||

| Other income, net |

1.2 | — | 0.3 | 0.1 | 0.2 | 0.6 | 0.6 | |||||||||||||||||||||

| Income (loss) before income taxes |

20.3 | 9.8 | (57.3 | ) | (74.2 | ) | (65.1 | ) | (28.8 | ) | 6.2 | |||||||||||||||||

| Income taxes |

— | (0.1 | ) | — | — | — | — | (0.1 | ) | |||||||||||||||||||

18

Table of Contents

| Six months ended June 30, |

Year ended December 31, | |||||||||||||||||||||||||||

| Summary Consolidated Statements of Income Data: | 2019 | 2018 | 2018 | 2017 | 2016 | 2015 | 2014 | |||||||||||||||||||||

| (Expressed in millions of U.S. dollars, except for per share data) | ||||||||||||||||||||||||||||

| Net income (loss) |

20.3 | 9.7 | (57.3 | ) | (74.2 | ) | (65.1 | ) | (28.8 | ) | 6.1 | |||||||||||||||||

| Earnings allocated to Series B Preferred Shares |

(1.5 | ) | (1.5 | ) | (3.1 | ) | (3.1 | ) | (3.1 | ) | (3.1 | ) | (1.1 | ) | ||||||||||||||

| Net income (loss) available to common shareholders |

18.8 | 8.2 | (60.4 | ) | (77.3 | ) | (68.2 | ) | (31.9 | ) | 5.0 | |||||||||||||||||

| Net income (loss) per Class A common share, in $ |

||||||||||||||||||||||||||||

| Basic and diluted |

0.82 | 1.36 | (7.42 | ) | (12.89 | ) | (11.39 | ) | (5.36 | ) | 0.8 | |||||||||||||||||

| Weighted average number of Class A common shares outstanding |

||||||||||||||||||||||||||||

| Basic and diluted in millions |

9.94 | 6.0 | 6.5 | 6.0 | 6.0 | 6.0 | 6.0 | |||||||||||||||||||||

| Net income per Class B common share, in $ |

||||||||||||||||||||||||||||

| Basic and diluted |

Nil | Nil | Nil | Nil | Nil | Nil | Nil | |||||||||||||||||||||

| Weighted average number of Class B common shares outstanding |

||||||||||||||||||||||||||||

| Basic and diluted in millions |

Nil | 0.9 | 0.9 | 0.9 | 0.9 | 0.9 | 0.9 | |||||||||||||||||||||

| Dividend per Class A common share in $ |

— | — | — | — | — | 0.02 | — | |||||||||||||||||||||

| Weighted average number of Class C preferred shares outstanding |

||||||||||||||||||||||||||||

| Basic and diluted in millions |

13.0 | Nil | 1.6 | Nil | Nil | Nil | Nil | |||||||||||||||||||||

| Net income (loss) per Class C preferred share, in $ |

||||||||||||||||||||||||||||

| Basic and diluted income (loss) |

0.4 | Nil | (7.4 | ) | Nil | Nil | Nil | Nil | ||||||||||||||||||||

| Statement of cash flow |

||||||||||||||||||||||||||||

| Net cash from Operating Activities |

$ | 36.6 | $ | 20.7 | $ | 47.7 | $ | 66.9 | $ | 71.6 | $ | 62.3 | $ | 60.9 | ||||||||||||||

| Net cash provided by (used in) Investing Activities |

(26.0 | ) | (12.8 | ) | 24.3 | (4.9 | ) | (6.9 | ) | (101.2 | ) | (80.1 | ) | |||||||||||||||

| Net cash (used in) provided by Financing Activities |

(15.4 | ) | (11.5 | ) | (55.2 | ) | (42.9 | ) | (64.1 | ) | 59.2 | 27.9 | ||||||||||||||||

| As of June 30, |

As of December 31, | |||||||||||||||||||||||||||

| 2019 | 2018 | 2018 | 2017 | 2016 | 2015 | 2014 | ||||||||||||||||||||||

| Balance sheet data (at period end) |

||||||||||||||||||||||||||||

| Total current assets |

99.5 | 76.5 | 99.0 | 77.4 | 57.1 | 57.6 | 36.7 | |||||||||||||||||||||

| Total vessels in operation |

1,118.0 | 595.3 | 1,112.8 | 586.5 | 707.3 | 838.4 | 826.2 | |||||||||||||||||||||

| Total assets |

1,236.3 | 671.8 | 1,233.5 | 675.9 | 777.2 | 904.9 | 873.7 | |||||||||||||||||||||

| Debt (current and non-current portion) |

865.2 | 390.9 | 877.2 | 398.5 | 419.9 | 478.1 | 401.9 | |||||||||||||||||||||

| Series B and C Preferred Shares |

— | — | — | — | — | — | — | |||||||||||||||||||||

| Class A and B common shares |

0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | |||||||||||||||||||||

| Shareholders’ equity |

335.2 | 260.1 | 316.4 | 251.6 | 328.9 | 395.8 | 438.1 | |||||||||||||||||||||

| Other data |

||||||||||||||||||||||||||||

| Number of vessels in operation at period end |

39 | 19 | 38 | 18 | 18 | 18 | 18 | |||||||||||||||||||||

| Ownership days |

6,912 | 3,271 | 7,675 | 6,570 | 6,588 | 6,893 | 6,270 | |||||||||||||||||||||

| Utilization |

96.9 | % | 98.4 | % | 98.7 | % | 98.4 | % | 98.4 | % | 99.6 | % | 98.0 | % | ||||||||||||||

19

Table of Contents

| (1) | On November 15, 2018, we completed a strategic combination with Poseidon Containers, acquiring 20 containerships, one of which, the Argos, was contracted to be sold which sale was completed in December 2018 (the “Poseidon Transaction”). The consideration given for the acquisition of the net assets was 3,005,603 Class A common shares and 250,000 Series C perpetual convertible preferred shares of par value $0.01 (the “Series C Preferred Shares”). Each Series C preferred share carries 38.75 votes and they are convertible in certain circumstances to 12,955,187 Class A common shares. References herein to “GSL Fleet” are to the 19 ships that were owned by us prior to the consummation of the Poseidon Transaction, and references to “Poseidon Fleet” are to the 19 ships that were acquired by us upon consummation of the Poseidon Transaction, excluding the Argos. |

| (2) | On January 2, 2019, as a consequence of the completion of the Poseidon Transaction, all of our issued and outstanding Class B common shares converted one-for-one into Class A common shares. On March 25, 2019, we effected a one-for-eight reverse stock split of our Class A common shares, which our shareholders authorized at our special meeting of shareholders held on March 20, 2019. There was no change to the trading symbol, number of authorized shares, or par value of our Class A common shares in connection with the reverse stock split. All share and per share amounts disclosed in this prospectus give effect to the reverse stock split retroactively, for all periods presented. |

Non-U.S. GAAP Financial Measures

To supplement our financial information presented in accordance with U.S. GAAP, we use certain “non-GAAP financial measures” as such term is defined in Regulation G promulgated by the SEC. Generally, a non-GAAP financial measure is a numerical measure of a company’s operating performance, financial position or cash flows that excludes or includes amounts that are included in, or excluded from, the most directly comparable measure calculated and presented in accordance with U.S. GAAP. We believe that the presentation of these measures provides investors with greater transparency and supplemental data relating to our financial condition and results of operations, and therefore a more complete understanding of factors affecting our business than U.S. GAAP measures alone. In addition, we believe that the presentation of these matters is useful to investors for period-to-period comparison of results as the items may reflect certain unique and/or non-operating items such as impairment charges, contract termination costs or items outside of our control.

We believe that the presentation of the following financial measures are useful to investors because they are frequently used by securities analysts, investors and other interested parties in the evaluation of companies in our industry. Adjusted EBITDA, Adjusted EBITDA Margin and Contracted Adjusted EBITDA are not defined in U.S. GAAP and should not be considered to be an alternative to net income or any other financial metric required by such accounting principles.

Non-U.S. GAAP measures

Adjusted EBITDA and Contracted Adjusted EBITDA are presented herein both on a historic basis and on a forward-looking basis in certain instances. We have not provided a reconciliation of any such forward looking non-U.S. GAAP financial measure to the most directly comparable U.S. GAAP measure because such U.S. GAAP financial measures on a forward-looking basis are not available to us without unreasonable effort.

Adjusted EBITDA

Adjusted EBITDA represents net income available to common shareholders before interest income and interest and other financial expense, income taxes, depreciation and amortization and earnings allocated to preferred shares. Adjusted EBITDA is a non-U.S. GAAP quantitative measure used to assist in the assessment of our operations. We believe that the presentation of Adjusted EBITDA is useful to investors because it is frequently used by securities analysts, investors and other interested parties in the evaluation of companies in our industry.

20

Table of Contents

(Expressed in millions of U.S. dollars)

| Six months ended | ||||||||||

| June 30, 2019 |

June 30, 2018 |

|||||||||

| Net income available to Common Shareholders |

18.8 | 8.2 | ||||||||

| Adjust: |

Depreciation and amortization |

21.7 | 16.3 | |||||||

| Interest income |

(0.8 | ) | (0.6 | ) | ||||||

| Interest and other financial expense |

38.1 | 21.5 | ||||||||

| Income taxes |

- | 0.1 | ||||||||

| Earnings allocated to preferred shares |

1.5 | 1.5 | ||||||||

|

|

|

|

|

|||||||

| Adjusted EBITDA |

79.3 | 47.0 | ||||||||

|

|

|

|

|

|||||||

Adjusted EBITDA Margin

Adjusted EBITDA Margin represents the Adjusted EBITDA for a period expressed as percentage of operating revenue for the same period.

| (Expressed in millions of U.S. dollars) | Six months ended | |||

| June 30, 2019 | ||||

| Operating revenues |

127.6 | |||

| Adjusted EBITDA |

79.3 | |||

|

|

|

|||

| Adjusted EBITDA Margin |

62.2 | % | ||

Contracted Adjusted EBITDA

Contracted Adjusted EBITDA represents our contracted future revenue multiplied by the Adjusted EBITDA Margin.

21

Table of Contents

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements. Forward-looking statements provide our current expectations or forecasts of future events. Forward-looking statements include statements about our expectations, beliefs, plans, objectives, intentions, assumptions and other statements that are not historical facts. Words or phrases such as “anticipate,” “believe,” “continue,” “estimate,” “expect,” “intend,” “may,” “ongoing,” “plan,” “potential,” “predict,” “project,” “will” or similar words or phrases, or the negatives of those words or phrases, may identify forward-looking statements, but the absence of these words does not necessarily mean that a statement is not forward-looking. Examples of forward-looking statements in this prospectus include, but are not limited to, statements regarding our disclosure concerning our operations, cash flows, financial position, dividend policy, the anticipated benefits of our strategic transaction with Poseidon Containers, and the likelihood of success in acquiring additional ships to expand our business.

Forward-looking statements appear in a number of places in this prospectus and in our Annual Report on Form 20-F for the year ended December 31, 2018, filed with the Commission on March 29, 2019, as updated by annual, quarterly and other reports and documents we file with the Commission after the date of this prospectus and that are incorporated by reference herein.

Forward-looking statements are subject to known and unknown risks and uncertainties and are based on potentially inaccurate assumptions that could cause actual results to differ materially from those expected or implied by the forward-looking statements. Our actual results could differ materially from those anticipated in forward-looking statements for many reasons, including the factors described in “Risk Factors” in this prospectus. The risks described under “Risk Factors” are not exhaustive. Other sections of this prospectus describe additional factors that could adversely affect our results of operations, financial condition, liquidity and the development of the industries in which we operate. New risks can emerge from time to time, and it is not possible for us to predict all such risks, nor can we assess the impact of all such risks on our business or the extent to which any risks, or combination of risks and other factors, may cause actual results to differ materially from those contained in any forward-looking statements. Accordingly, you should not unduly rely on these forward-looking statements, which speak only as of the date of this prospectus. We undertake no obligation to publicly update or revise any forward-looking statement to reflect circumstances or events after the date of this prospectus or to reflect the occurrence of unanticipated events. You should, however, review the factors and risks we describe in the reports we will file from time to time with the Commission after the date of this prospectus.

22

Table of Contents

An investment in our Class A common shares involves a high degree of risk. Before making an investment in our Class A common shares, you should carefully consider all of the information included or incorporated by reference into this prospectus, including the risks described herein and in “Item 3. Key Information—D. Risk Factors” in our 2018 Annual Report, which is incorporated by reference herein. The occurrence of one or more of those risk factors could adversely impact our business, financial condition or results of operations.

We cannot assure you if and when we will pay dividends on our Class A common shares.

We are not currently paying dividends on our Class A common shares. Subject to the limitations contained in the indenture governing our 2022 notes and other contractual obligations, we may resume the distribution of a portion of our cash flow to our shareholders, while retaining the remaining cash flow for costs such as drydockings, reinvestment in our business, funding ship or fleet acquisitions, making debt repayments and for other purposes, as determined by our board of directors. The timing and amount of any dividends declared will depend on, among other things (a) our results of operations, financial condition, cash flow and cash requirements, (b) our liquidity, including our ability to obtain debt and equity financing on acceptable terms as contemplated by our ship acquisition strategy, (c) restrictive covenants in our existing and future debt instruments and (d) provisions of Marshall Islands law. The declaration and payment of dividends is also subject at all times to the discretion of our board of directors.

The container shipping industry is highly volatile, and we cannot predict with certainty the amount of cash, if any, that will be available for distribution as dividends in any period. Also, there may be a high degree of variability from period to period in the amount of cash, if any, that is available for the payment of dividends. The amount of cash we generate from operations and the actual amount of cash we will have available for dividends in each quarter will vary based upon, among other things:

| • | the charter-hire payments we obtain from our charters as well as the rates obtained upon the expiration of our existing charters; |

| • | acquisition of additional ships or significant capital improvements; |

| • | the timing of scheduled drydockings; |

| • | the timing of interest payments, scheduled debt amortization payments and other payments that might be due under our debt facilities; |

| • | delays in the delivery of newbuilding ships, if any, and the beginning of payments under charters relating to those ships; |

| • | the level of our operating costs, such as the costs of crews, lubricants and insurance; |

| • | the number of unscheduled off-hire days for our fleet and the timing of, and number of days required for, scheduled dry-docking of our containerships; |

| • | any idle time after one charter expires until a new charter is agreed or the ship is disposed of, should a new charter not be agreed; |

| • | unexpected repairs to, or required expenditures on, ships or dry-docking costs in excess of those anticipated; |

| • | the loss of a ship; |

| • | prevailing global and regional economic and political conditions; |

| • | changes in interest rates; |

| • | the effect of governmental regulations and maritime self-regulatory organization standards on the conduct of our business; |

23

Table of Contents

| • | changes in the basis of taxation of our activities in various jurisdictions; |

| • | modification or revocation of our dividend policy by our board of directors; and |

| • | the amount of any cash reserves established by our board of directors. |

The amount of cash we generate from our operations may differ materially from our net income or loss for the period, which will be affected by non-cash items. We may incur other expenses or liabilities that could reduce or eliminate the cash available for distribution as dividends.

In addition, Marshall Islands law generally prohibits the payment of dividends other than from surplus (retained earnings and the excess of consideration received from the sale of shares above the par value of the shares) or if there is no surplus, from the net profits for the current and prior fiscal years, or while a company is insolvent or if it would be rendered insolvent by the payment of such a dividend. We may not have sufficient surplus or net profits in the future to pay dividends, and our subsidiaries may not have sufficient funds, surplus or net profits to make distributions to us. As a result of these and other factors, we may not be able to pay dividends during periods when we record losses and may not pay dividends during periods when we record net income. We can give no assurance that dividends will be paid in the future.

There may be a substantial number of our Class A common shares available for sale in the future that may adversely affect the market price of our Class A common shares.

On the closing of the Poseidon Transaction, we issued 3,005,603 Class A common shares and 250,000 Series C Preferred Shares, which are convertible into 12,955,187 Class A common shares upon the occurrence of certain events. Further, in connection with the Poseidon Transaction, pursuant to an Amended and Restated Registration Rights Agreement, we registered for resale all Class A common shares, including those issuable on conversion of the Series C Preferred Shares, held by affiliates of Kelso, CMA CGM, George Giouroukos (our Executive Chairman) through Management Investor Co., Michael S. Gross (our former Chairman and a director) and MAAS Capital as of the closing of the Poseidon Transaction. In September 2019, Kelso agreed to convert its Series C Preferred Shares upon the Company’s repayment of its 9.875% First Priority Secured Notes due 2022. The registration and availability of such a significant number of securities for trading in the public market may have a material adverse effect on the market price of our Class A common shares.

The price of our securities may be volatile.

The price of our Class A common shares may be volatile and may fluctuate due to factors such as:

| • | actual or anticipated fluctuations in our quarterly revenues and results of operations and those of publicly held containership owners or operators; |

| • | market conditions in the container shipping industry; |

| • | perceived counterparty risk; |

| • | shortfalls in our operating results from levels forecasted by securities analysts; |

| • | announcements concerning us or other containership owners or operators; |

| • | mergers and strategic alliances in the shipping industry; |

| • | changes in government regulation including taxation; and |

| • | the general state of the securities markets. |

The container shipping industry has been highly unpredictable and volatile. The market for common shares in companies operating in container shipping industry may be equally volatile.

24

Table of Contents

Future sales of our common stock could cause the market price of our common stock to decline.

Sales of a substantial number of shares of our common stock in the public market, or the perception that these sales could occur, may depress the market price for our common stock. These sales could also impair our ability to raise additional capital through the sale of our equity securities in the future.

Subject to the rules of the NYSE, in the future, we may issue additional shares of common stock, and other equity securities of equal or senior rank, without shareholder approval, in a number of circumstances. The issuance by us of additional shares of common stock or other equity securities of equal or senior rank would have the following effects:

| • | our existing shareholders’ proportionate ownership interest in us may decrease; |